Solid Labor Market Gains, with Even More Room for Improvement

Solid Labor Market Gains, with Even More Room for Improvement

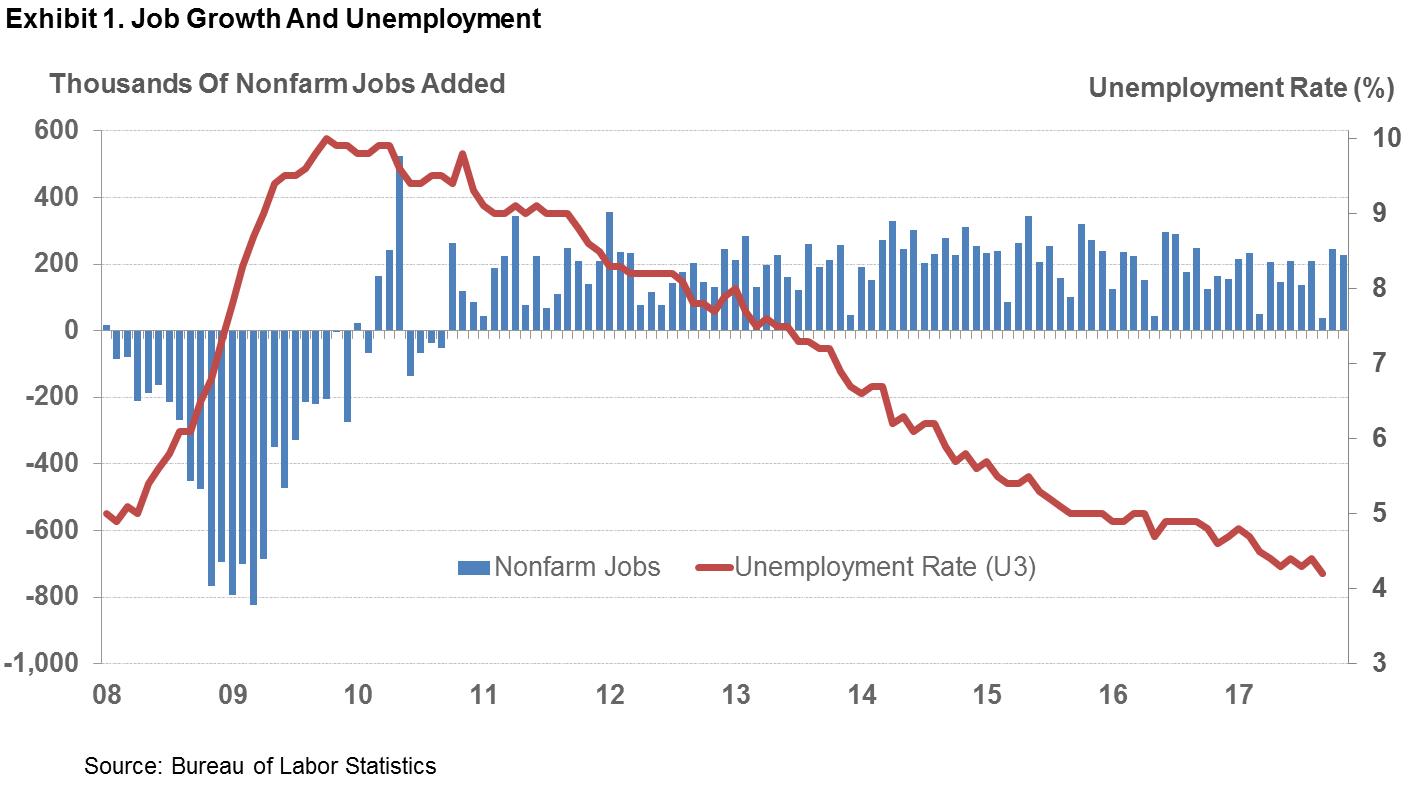

Nonfarm payroll employment marched further forward in November, adding 228,000 jobs and also revising October’s jobs upward by 3,000, as reported by the Dept. of Labor on Friday. The average number of jobs added per month in 2017 now stands at 175,000, a slowdown from the same period in 2016 but still defying expectations for job growth as the economy enters what is widely believed to be a state of full employment.

The unemployment rate held steady at 4.1%, as the growth in the labor force over the month added not only to the number of employed but also to the number of unemployed.

The rosy employment picture buttresses the case for optimism as economic conditions continue to swing to the upside. Consumer confidence levels are reaching new heights (in spite of a small dip in November), and household balance sheets continue to improve. Meanwhile, increases in equity and home prices also add to the buoyancy among market participants. Expectations for economic growth settling in above 3% are growing given recent data.

With an economy at full employment — meaning that everyone seeking a job is able to find one — how much room can there be for continued job growth above the rate of population growth?

November’s report shows that jobs were added at an annualized rate of 1.9%, more than twice the rate of population growth. With an unchanged unemployment rate, this indicates that individuals are still being drawn into the labor force.

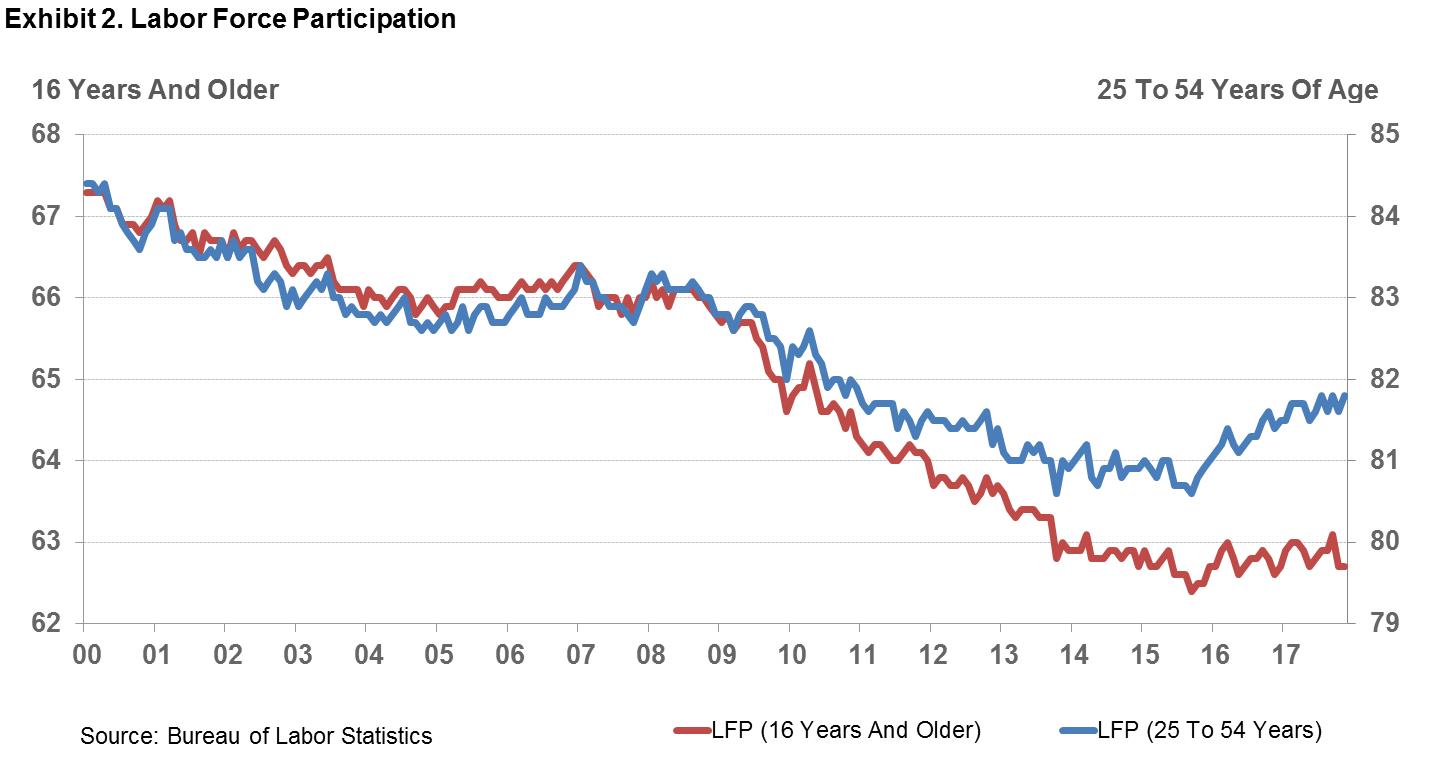

And there may well be a surplus still waiting to be gainfully employed. Labor force participation has been on a steady decline since the end of the recession and has only recently begun flattening out, sitting at 62.7% in this report compared to the pre-recession high of 66% and more than 67% in 2000.

To put these numbers in perspective, an increase of half of one percentage point in labor participation equals almost 1.3 million additional available workers. If the economy were to return to a higher participation rate, there could be plenty of available workers for employers to add jobs without further tightening the labor market.

An encouraging sign is that the labor force participation rate of the prime-aged working population (those between the ages of 25 and 54) has been on the rise after years of steady declines. Accounting for almost two-thirds of the labor force, this is the largest cohort and the most watched, and still has some way to go before reaching levels that were seen in the earlier years of the century.

Wage growth remains muted and continues to weigh on our optimism, but pessimism and caution may be misplaced. The lack of consistent and generous wage growth is clearly a function of the industries and occupations that are growing.

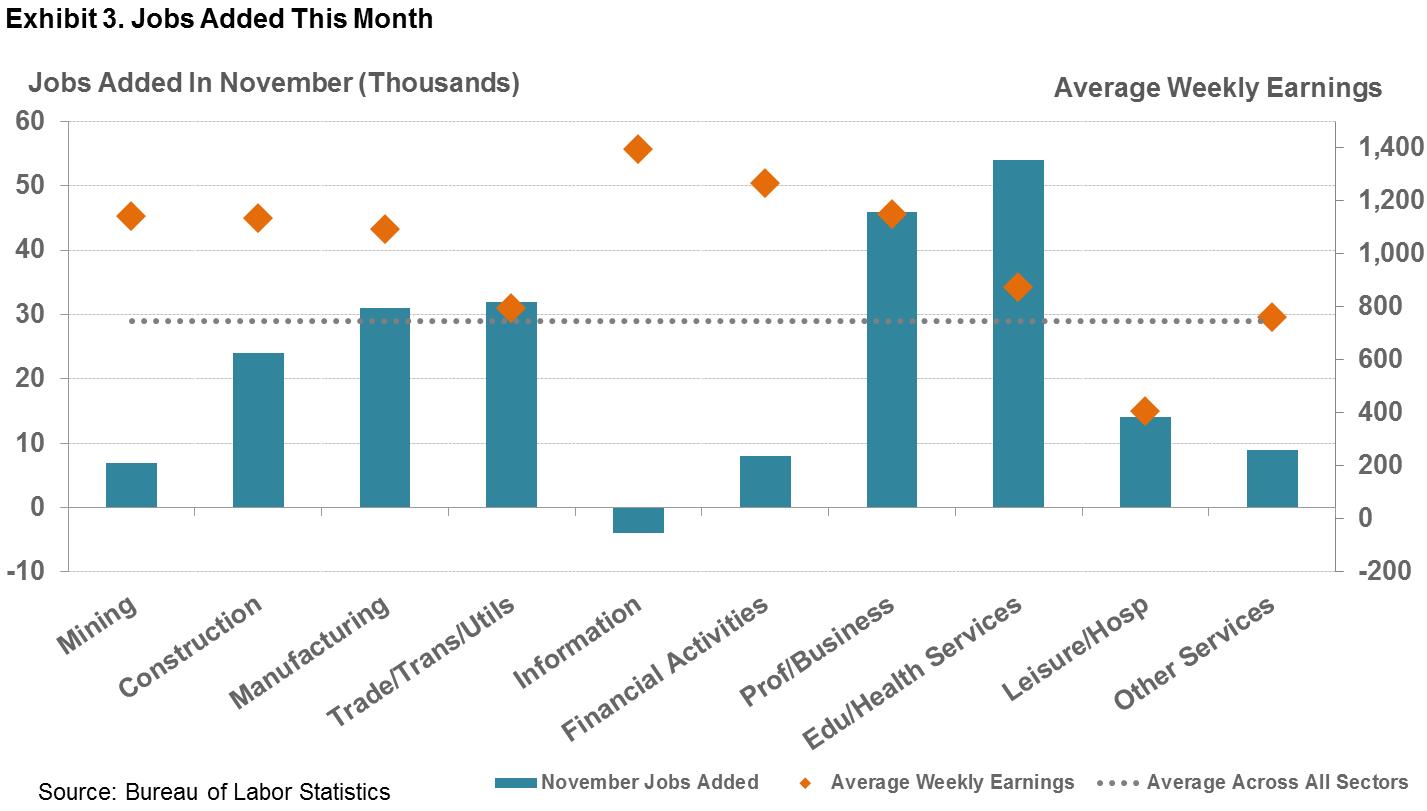

Jobs added in November were distributed by industry sector as shown in Exhibit 3 below. The highest number of jobs was added in leisure and hospitality, many of which are typically part-time jobs with modest wages. Almost 40% of the jobs added in professional and business services were temporary positions, which provide limited tenure and modest wages.

High-wage jobs such as those in information, financial activities, mining, construction, and manufacturing accounted for smaller job gains, dampening the potential for overall earnings growth.

As we noted last month, the picture continues to be one of healthy earnings in a handful of industries that add, in the aggregate, fewer jobs, and weak earnings in sectors that add, in the aggregate, many more jobs.

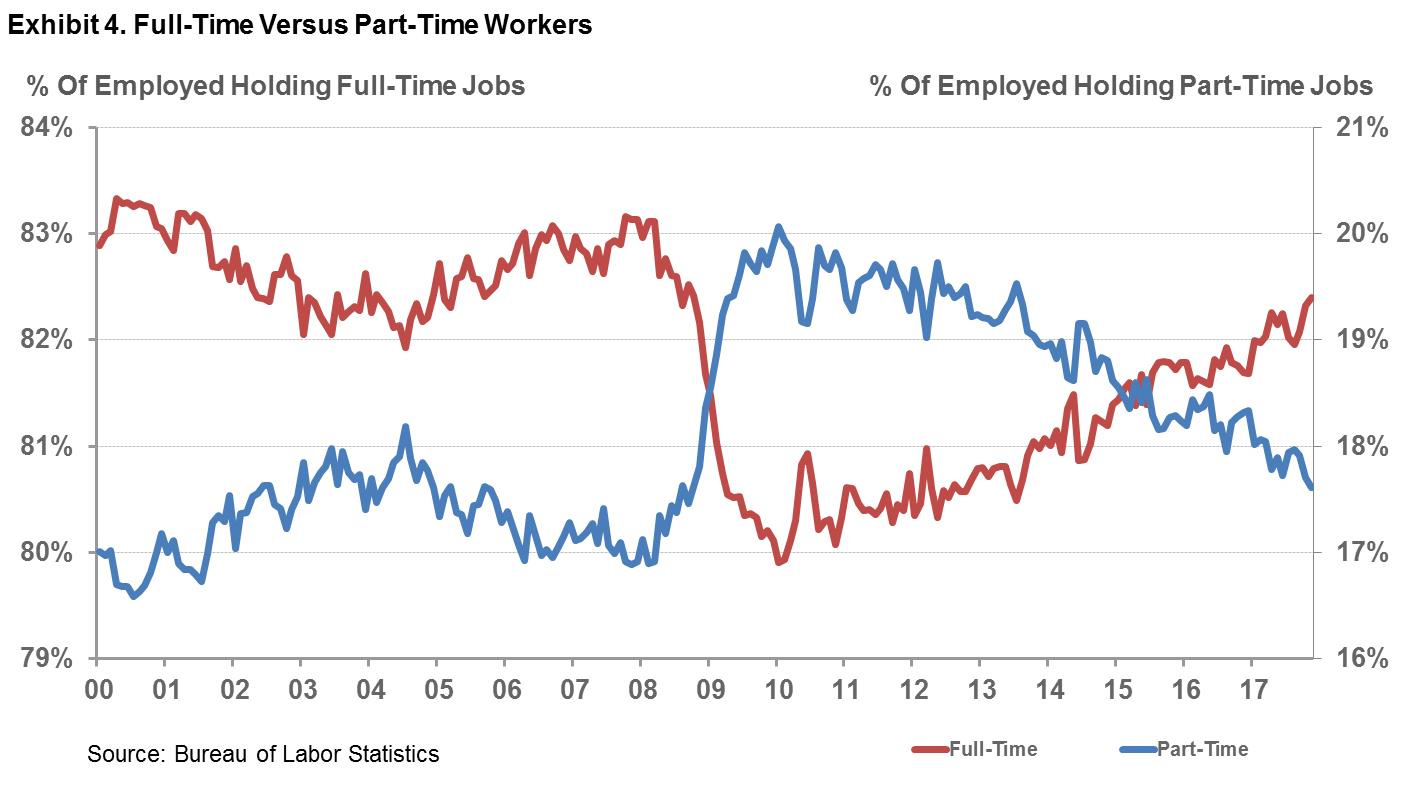

One cause of low wages and weak wage growth is certainly related to the job status of workers. Retail jobs, temporary jobs, and employment in the leisure and hospitality industry sector and in social assistance are more likely to be part-time and subject to lower wages. During the recession, with jobs being lost across the economy, part-time positions grew as a percentage of all jobs from 17% to over 20%.

Since the end of the recession, the full-time job market is continuing to gain momentum. These positions are more likely to enjoy benefits such as paid time off for vacation and sick leave and to receive health insurance coverage and benefits – added employment compensation which is not included in the earnings data. With the balance between full-time jobs and part-time jobs reverting to pre-recession levels, we are likely to see overall earnings grow.

The flip side of tepid wage growth is that labor costs may place less of a burden on profit margins. With plenty of potential labor available for further job increases, moderated labor costs, and price increases kept in check, there would seem to be less motivation for the Federal Reserve to seek faster interest rate increases, potentially choking off what is arguably a solid and sustainable economy.

Barring any unforeseen event, there are few clouds on the horizon in this fair-weather environment.

Source: Solid Labor Market Gains, with Even More Room for Improvement